Somewhere right now, a number between 300 and 850 is quietly shaping your life. It determines whether you get the mortgage, the apartment, the car loan, or the business line of credit. It follows you from city to city, job to job, decade to decade. And most Americans have no idea where it came from.

The credit score feels like a product of the digital age — clean, algorithmic, objective. But its roots stretch back to the grubby, deeply personal world of 19th-century American commerce, where merchants kept handwritten ledgers on their customers' characters, and traveling salesmen traded reputation gossip like currency.

When Credit Was Just a Conversation

In early America, extending credit was a deeply local act. A general store owner in rural Ohio knew his customers personally. He knew who paid on time, who made excuses, who had a drinking problem that made them a bad risk. He didn't need a formula. He had a community.

But as American commerce expanded westward and cities grew larger, that personal knowledge became impossible to maintain. Merchants were suddenly selling to strangers. Manufacturers were shipping goods to retailers they'd never met, in towns they'd never visited, on the promise of future payment. The old system — trust built through years of personal interaction — couldn't scale.

Somebody had to start keeping track.

The Traveling Men With Notebooks

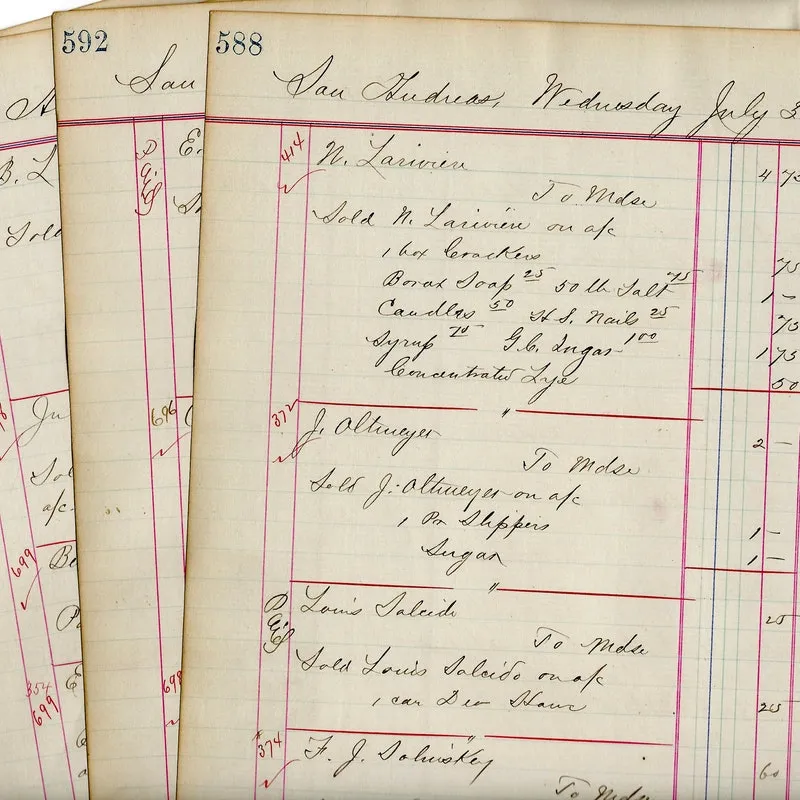

In the mid-1800s, a loose network of traveling salesmen and commercial agents began doing something that would look familiar to anyone who's ever left a Yelp review: they started writing things down. Not about products, but about people. Who was good for it. Who had a history of slow payment. Who'd gone bankrupt once and quietly reopened under a different name.

These notes were informal, often scrawled on scraps of paper or in small leather notebooks. But they circulated. Salesmen shared them with colleagues. Merchants compared notes at trade fairs. Slowly, a shadow information network emerged — one that could make or break a business owner's ability to buy on credit.

In 1841, a New York silk merchant named Lewis Tappan formalized the concept. Frustrated by the losses he'd sustained from customers who turned out to be bad credit risks, Tappan founded the Mercantile Agency — widely considered the first credit reporting bureau in the world. He hired correspondents across the country: lawyers, local businessmen, anyone with an ear to the ground. Their job was to report back on the financial character of local merchants.

The reports were blunt, often biased, and sometimes spectacularly wrong. They included assessments of a person's moral character, sobriety, and family background alongside their financial history. A man who drank too much, or whose wife spent extravagantly, or who attended the wrong church might find his credit rating quietly tanked. The system was as much about social judgment as financial data.

From Ledgers to Algorithms

For the next century, credit reporting remained a patchwork of local bureaus and regional agencies, each maintaining their own files and standards. The information was inconsistent, often discriminatory, and almost completely invisible to the people it described. You could be denied a loan and never know why.

The pivot toward something more systematic came from an unlikely corner: a small engineering consultancy in San Jose, California. In 1956, engineer Bill Fair and mathematician Earl Isaac founded the Fair Isaac Corporation with a simple premise — that credit risk could be predicted mathematically, using historical data rather than personal judgment. Their product, the FICO score, didn't gain immediate traction. Banks were skeptical. The idea that a formula could replace a loan officer's instincts felt cold and, frankly, a little insulting to the professionals involved.

But the math kept proving itself right. By the late 1980s, major lenders were starting to adopt FICO scores as a standardized measure. When Freddie Mac began recommending their use for mortgage decisions in 1995, the game was effectively over. The score had become the standard.

The System That Runs on Your History

Today's FICO score is built from five categories: payment history, amounts owed, length of credit history, new credit, and credit mix. It sounds clinical and neutral — and compared to 19th-century assessments of a man's sobriety and churchgoing habits, it genuinely is. But the system still carries echoes of its origins.

For decades, credit reporting bureaus included information about race, gender, and neighborhood — factors that had nothing to do with an individual's financial behavior and everything to do with systemic discrimination. The Fair Credit Reporting Act of 1970 began cleaning this up, and the Equal Credit Opportunity Act of 1974 banned discrimination based on race, sex, and national origin. But researchers continue to document disparities in credit scores across racial and income lines that suggest the system's legacy isn't entirely scrubbed.

The Number That Follows You Everywhere

What began as a merchant's grudge list has become one of the most consequential numbers in American life. Your credit score affects not just loans and credit cards but rental applications, insurance premiums, and in some states, even job applications. It's a financial reputation score in the most literal sense — a direct descendant of those handwritten notebooks passed between salesmen on 19th-century trade routes.

The carnival barker analogy isn't far off. The original credit reporters were selling confidence — convincing merchants that they could know a stranger well enough to extend trust. The FICO score does the same thing, just with better math and fewer personal grudges.

Next time you check your credit score, you're looking at 180 years of American commerce compressed into three digits. It started as gossip. It became infrastructure.